Health Insurance After Death of A Spouse: Your Options, Deadlines, and Next Steps

Taming the beast of healthcare bureaucracy after the loss of a spouse can be frustrating and overwhelming. But with the right tools and knowledge, it’s possible. Here’s how to go about it.

Losing a spouse is overwhelming. The grief alone is more than anyone should have to carry, and yet within days — sometimes hours — the practical world comes knocking. There are bills that need to be paid, and accounts that need to be closed or transferred. Paperwork, paperwork, and…more paperwork.

Somewhere in that unwanted to-do list: health insurance.

Health coverage is one of the most time-sensitive financial issues a surviving spouse faces. The deadlines are real, the consequences of missing them can be expensive, and the options available to you depend heavily on your age, your situation, and which spouse held the coverage.

Today, we’re going to walk through major scenarios, what your choices are, and when you have to act.

➡️Speaking of pressing deadlines: if you’re looking for help on it, we've written a separate guide on what to do with life insurance money after your spouse dies that may help.)

Health Insurance After Death of a Spouse: Two Big Variables

Before getting into specifics, here are two important questions:

1. How old are you?

👉 If you’re under 65, your primary options are through COBRA, the ACA Marketplace, your own employer (if offered), and CHIP for children. We’ll get into these next.

👉 At 65 and older, Medicare is what you’ll likely focus on. (Exceptions exist: some people delay Medicare enrollment if they're still covered through an employer plan, and a small number of lower-income individuals may be covered primarily through Medicaid. In those cases, you’ll want to contact the human resources department of whosever employer offers the insurance, or get in touch with your state’s Medicaid office and speak with a benefits counselor.)

2. Whose plan were you on? If you were covered under your late spouse's employer plan, you've lost coverage and need to act quickly. If your spouse was covered under your plan, your situation is generally simpler.

If You're Under 65

The median age of a widow is age 59. That means for most people, you’re left with a wider array of options, making their health insurance coverage decision more complicated. Here are the most common scenarios a widow under age 65 will face.

Scenario 1: Your Late Spouse Carried the Coverage Through Their Job

When an employee passes away, their employer-sponsored health insurance ends — however, not necessarily immediately. Some end on the date of death; however, it’s more common for them to continue through the end of month of death. The best way to find out is to contact the HR department, and ask them what the plan says.

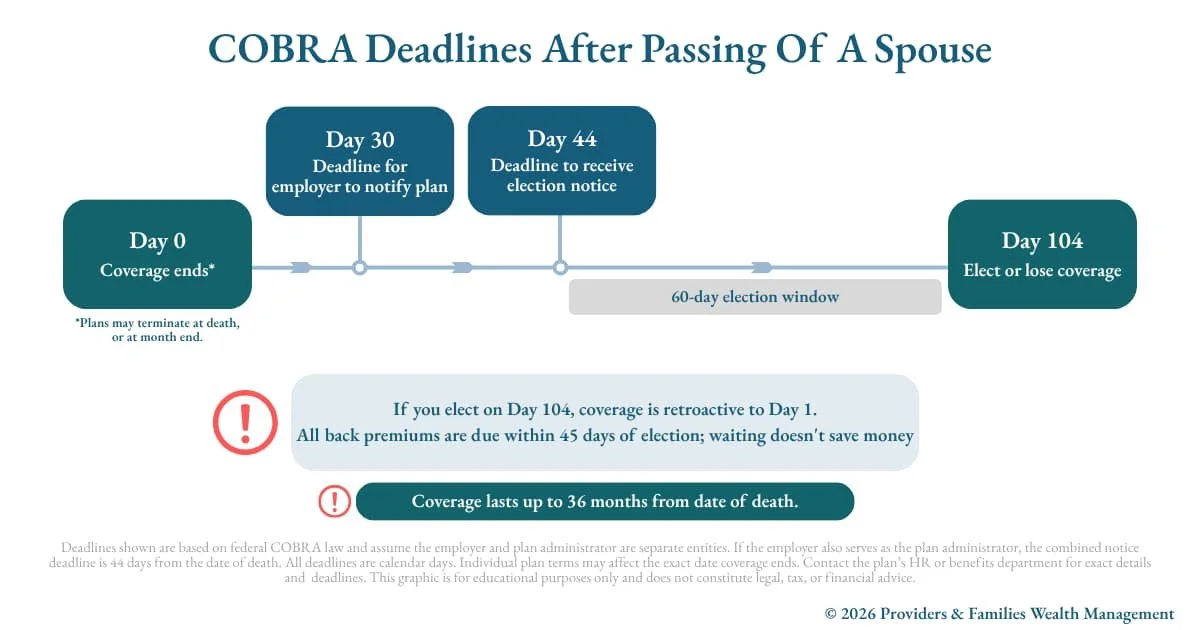

Regardless of when it ends, it will — soon. That means you (and any dependent children covered under that plan) lose coverage. But, federal law states that this is a qualifying event which triggers your right to COBRA continuation coverage. There’s a timeline that’s attached to this, and it’s more layered than many people realize, because there are actually two clocks running at once.

How the COBRA Deadline Works After a Spouse's Death

First, the employer has 30 days from your spouse's death to notify the health plan administrator. This typically starts with a notification from you, the surviving spouse. Then the plan administrator has 14 days from receiving that notification to send you an election notice — the paperwork explaining your right to continue coverage and what it will cost. If the employer is also the plan administrator (common in smaller companies), they get the combined 44-day window.

➡️NOTE: If you don’t receive an election notice within 44 days, it’s wise to reach back out to your late spouse’s employer. If those deadlines pass with no communication, you can file a complaint with the U.S. Department of Labor's Employee Benefits Security Administration.

Once you receive that election notice, you have 60 days to decide whether to elect COBRA. This 60-day window doesn’t start until you receive the election notice. If you’re in a hurry to receive it faster, or if you’ve delayed acting until close to the end of that window and can’t locate the election notice (understandable at a time like this), call human resources to see if they can accommodate you by emailing you the election notice.

If you elect COBRA, your coverage is retroactive to the date coverage ended, so there's no gap even if you take a few weeks to decide. You also have 45 days after electing COBRA to make your first premium payment.

Another thing to know is that COBRA after the death of a spouse lasts up to 36 months — not the 18 months associated with job loss. If you have dependent children who qualify for coverage on that plan, three years of coverage can potentially carry them to an age when they have coverage options of their own — either through an employer, or at age 26, when they’ll need to find their own plan.

➡️Related: If you’re wondering, “why does any of this work this way,” you’re not alone. Read about the Consolidated Omnibus Budget Reconciliation Act of 1985 here.

What COBRA Will Cost You

The downside of COBRA is its often surprising price tag. When your spouse was employed, their employer was likely covering a significant share of the premium. Under COBRA, you pay the full premium plus a 2% administrative fee — not ideal while adjusting to a reduced income, to say the least. Monthly costs can easily run $400 to $700 per month for an individual, and $1,200 to $2,000 or more for family coverage.

COBRA vs. your original plan

COBRA is the same plan — only the billing changes.

| Original employer plan | COBRA continuation | |

|---|---|---|

| Network of doctors | Same network | Same networkidentical |

| Deductible | Same deductible | Same deductibleidentical |

| Copays & coinsurance | Same copays | Same copaysidentical |

| Prescriptions covered | Same formulary | Same formularyidentical |

| Benefits & coverage | Full benefits | Full benefitsidentical |

| Who pays the premium | You + employer share the cost | You pay 100% + 2% admin feechanges |

| Monthly cost (individual) | ~$120/mo avg. employee share | ~$400–$700+/mo full premium (higher with dependents)changes |

| How long it lasts | As long as employed | Up to 36 months after death of spousechanges |

Average employee premium share based on KFF 2025 Employer Health Benefits Survey. Individual COBRA costs vary by plan and location.

This table is for educational purposes only and does not constitute legal, tax, or financial advice. Consult your plan administrator or a qualified advisor for information specific to your situation.

An additional heads-up: your deductible resets at the start of the employer's plan year, which is often January 1st. If your spouse died late in the year and your family already met the deductible, that resets when the new plan year begins, not one year from termination of previous coverage. If you have upcoming medical expenses, it’s wise to get in what you can before the reset happens.

Your Other Options: ACA Marketplace and Your Own Employer

Not only is COBRA not your only path, it's often not the most affordable or even logical option.

Because the death of a covered spouse is a qualifying life event, you have a 60-day special enrollment period to sign up for a plan through the ACA Marketplace at healthcare.gov. The 60 days runs from the date coverage actually ends. Note that this isn’t necessarily the date of death, since many plans run through the end of the month.

Marketplace plans may be significantly cheaper than COBRA, particularly if your income has been reduced substantially after your spouse's death. The Affordable Care Act caps premiums as a percentage of income for exchange plans, and depending on where your income lands, you may qualify for substantial subsidies. It's worth comparing both options before defaulting to COBRA out of familiarity.

If your own employer offers coverage and you weren't previously enrolled because you were on your spouse's plan, you also have a 30-day special enrollment window to join your employer's plan under HIPAA rules.That deadline is shorter than the marketplace window and easy to miss in the fog of grief — don't let it slip by.

What If a Medical Expense Comes Up Before You've Done Anything?

If your spouse died and you haven't yet contacted anyone, elected COBRA, or made any coverage decisions — you may still be covered for expenses incurred in the days immediately after the death. Your first call should be to the employer's HR or benefits department to confirm the exact date coverage will end.

Now here's what matters if a medical expense falls after coverage has lapsed but before you've elected COBRA: COBRA coverage is retroactive. If you elect COBRA within your 60-day window and pay all premiums owed, your coverage is treated as having been continuous from the date it would have otherwise ended. That means a medical expense incurred in the gap — say, on the 3rd of the following month when coverage ended on the 31st — can be covered retroactively once you elect and pay. You don't have to decide immediately just because a bill arrived.

Bottom line: if you got a medical bill for services you received during this 60-day window, and haven’t elected COBRA — that bill could still be covered, as long as you elect COBRA and pay back the premiums. But a medical bill that comes up during this window won’t be covered if you switch to an ACA plan, or any other non-COBRA plan.

Scenario 2: You Carried the Coverage — Your Spouse Was on Your Plan

If your late spouse was covered under your employer plan as a dependent, you're losing a dependent on your policy.

Your first call should still be to your HR department to notify them of the death and have your spouse removed from the plan. Good news here: your premium will likely decrease, since you'll now be covering only yourself (and children, if applicable).

Beyond that administrative step, your own coverage just continues uninterrupted. You don't face a gap or an enrollment deadline the way someone in Scenario 1 does. The main thing to keep in mind is that if you later change jobs, leave employment, or experience your own qualifying event down the road, the same COBRA and marketplace rules will apply to you at that point.

Health Insurance for Children After Losing a Parent

Whether the coverage was through your late spouse's employer or your own, dependent children have unique options.

If your children were on your late spouse's employer plan, they're in the same position you are — entitled to COBRA continuation for up to 36 months, and eligible for a marketplace plan during the 60-day special enrollment window. If you're moving them onto your employer plan, remember your 30-day HIPAA enrollment window.

What If You Can't Afford Coverage for the Kids?

This is where the Children's Health Insurance Program — CHIP — comes in. CHIP is a federal program administered state by state, so eligibility rules, income thresholds, and the enrollment experience vary depending on where you live.

In Pennsylvania, for example, CHIP covers children under age 19 who are Pennsylvania residents, U.S. citizens or qualified immigrants, currently uninsured, and whose household income falls within program guidelines. Children cannot be enrolled in any other health insurance — including employer-sponsored coverage — to qualify. CHIP is a standalone option for when private insurance isn't available or affordable.

Pennsylvania CHIP offers free coverage for lower-income families and low-cost coverage with modest premiums and copays for moderate-income families. Benefits are comprehensive: routine checkups, prescriptions, dental, and vision. Applications go through Pennsylvania's COMPASS system, which handles both CHIP and Medical Assistance (Medicaid) determinations together. If your income falls below CHIP thresholds, your child may be directed to Medical Assistance instead.

One of the most important things to know about CHIP — in Pennsylvania and nationally — is that there is no enrollment deadline or open enrollment period. Families can apply at any time of year. So even if you're still getting your bearings weeks after the loss, this door stays open.

Nationally, CHIP fills the gap between Medicaid income limits and private insurance affordability for children. Income limits and program specifics vary by state, but the core structure is the same: it's for families who earn too much for Medicaid but can't afford private insurance for their kids.

If You're 65 or Older: Health Insurance and Medicare After Losing a Spouse

Medicare operates on a different set of rules, and losing a spouse near or after age 65 raises questions that catch a lot of people off guard.

If You Were Both Already on Medicare

If both you and your spouse were enrolled in Medicare, your own coverage doesn't end with your spouse's death. Medicare is individual coverage — each person has their own enrollment and their own plan. What may need attention is your supplemental coverage situation (Medigap, Medicare Advantage, or Part D drug coverage) if any plan terms are affected by the loss of your spouse.

Notify Medicare and Social Security of your spouse's death so that records and billing can be updated. Beyond that, your Medicare continues. (Note that funeral homes typically notify the Social Security Administration, who then notifies Medicare.)

If You Were Covered Under Your Spouse's Employer Plan and Are Now Losing That Coverage

This is the highest-stakes scenario for Medicare-age widows and widowers.

Many people delay enrolling in Medicare Part B — and sometimes Part A — because they're covered under a working spouse's employer plan. Medicare allows this without penalty as long as that employer coverage is active. When it ends due to your spouse's death, the clock starts.

You qualify for a Medicare Special Enrollment Period. For Parts A and B, you have 8 months from the date the employer-sponsored coverage ends to enroll without triggering a late enrollment penalty.This is a more generous window than most people expect, but it's critical to use it — because the Part B late enrollment penalty adds 10% to your monthly premium for every full year you were eligible but didn't enroll, and that penalty is permanent for as long as you have Part B.

COBRA does not extend this 8-month window. If you elect COBRA as a bridge after your spouse's death, Medicare still treats employer-based coverage as having ended on the date of death (or the date coverage terminated). The 8-month clock doesn't pause because you're on COBRA. This is a costly misunderstanding — many widows arrive at the end of their COBRA period believing they still have time to enroll in Medicare, and find out they don't.

For Part D (prescription drug coverage), the window is even shorter — 63 days from the date you lose creditable drug coverage before a late enrollment penalty may apply.

Qualifying for Premium-Free Part A on Your Late Spouse's Work Record

Medicare Part A (hospital insurance) is premium-free for most people based on their own work history — 40 quarters, or roughly 10 years, of Medicare-covered employment. If you don't have sufficient work history of your own, you may be able to qualify based on your late spouse's record.

To do so, you generally need to have been married for at least nine months prior to your spouse's death, must not have remarried, and your late spouse must have had at least 40 quarters of Medicare-covered work. If those conditions are met, you can qualify for premium-free Part A at age 65.

Part B premiums are based on your individual income — your spouse's work history doesn't affect what you pay there — but you still need to enroll in Part B during your enrollment window.

Medigap and Medicare Advantage After a Spousal Loss

If you were on a Medicare Advantage or Medigap plan and your circumstances have changed, you generally have the ability to make plan changes during a special enrollment period triggered by loss of coverage. Contact your plan directly — the rules around Medicare Advantage and Medigap changes are more specific than Original Medicare enrollment and worth confirming with the plan or a licensed Medicare broker.

Electing COBRA after your spouse's death does not pause your Medicare enrollment clock. The 8-month window to enroll in Medicare Part B without a late enrollment penalty starts when employer coverage ends — not when COBRA ends.

This means you can elect COBRA and enroll in Part B at the same time. In fact, that's often the right move. Medicare becomes your primary coverage; COBRA acts as a secondary plan covering gaps. You'll pay a Part B premium, but you'll lock in your enrollment without a penalty.

If you miss your 8-month window, the penalty is permanent: 10% added to your Part B premium for every full year you delayed — for as long as you have Medicare. Even a single year of delay means paying meaningfully more every month for the rest of your life.

Not sure where you stand? A licensed Medicare broker or benefits counselor can help you map out your enrollment timeline before the window closes.

The Deadlines, Condensed

COBRA: Employer has 30 days to notify the plan administrator; administrator has 14 more days to send you the election notice (44 total if they're the same entity). You then have 60 days from receipt of that notice to elect. First payment due 45 days after election. Coverage lasts up to 36 months after a spouse's death.

ACA Marketplace: 60 days from loss of coverage. Runs concurrently with your COBRA decision window — you're comparing both at the same time.

Your own employer plan (HIPAA): 30 days from loss of coverage to request enrollment.

CHIP: No deadline. Apply any time of year.

Medicare Parts A and B: 8 months from the date employer-sponsored coverage ends. COBRA does not extend this window.

Medicare Part D: 63 days from loss of creditable drug coverage.

What about Medicaid?

If losing your spouse significantly reduces your household income, you may find yourself newly eligible for Medicaid— and if you have an adult child with a disability who is already on Medicaid, or who may qualify after this transition, it's worth knowing how the program works. Medicaid is a joint federal-state program for people with lower incomes and, in some cases, qualifying disabilities. Like CHIP, it has no open enrollment period — you can apply at any time through your state's Medicaid agency or through healthcare.gov. Eligibility rules vary by state, so what you qualify for in Pennsylvania may differ from another state. If you think you or a family member might qualify, the fastest way to find out is to contact CHIP and talk to a specialist.

A Few Final Thoughts

Navigating healthcare after the loss a spouse can feel like a maze. The deadlines are real and the consequences of missing them can follow you for years, so acting quickly matters even when acting quickly is the last thing you feel capable of.

That said, you don't have to figure this out alone. Your late spouse's HR department is legally required to send you COBRA information, and you can push them if they're slow. A financial advisor, benefits counselor, or health insurance broker can help you compare COBRA against marketplace options based on your actual income situation. An independent Medicare agent can help you navigate Medicare decisions, too.

If you're also navigating questions about retirement accounts, we've written about inherited IRA rules for surviving spouses — including when it makes sense to roll the account over versus keep it as an inherited IRA.

And if you're looking for a broader starting point, our resources for widows page has free resources and information for you.

You have options. Most of them have windows. Know your deadlines, take them seriously, and don’t be afraid to lean on knowledgeable resources for help if you need to.

About the author

Scot Whiskeyman, CFP® is co-founder of Providers & Families Wealth Management. Together with his wife and business partner Lindsey, they help widows navigate complex financial decisions with confidence and peace of mind.

A central Pennsylvania native, Scot lives in Carlisle, Pennsylvania with his wife Lindsey and their cats. Scot enjoys distance running and has completed 4 marathons, one ultramarathon, and countless other distance races.

Navigating health insurance after losing a spouse is one of many financial decisions that shouldn't have to fall on you alone. If you'd like to talk through your situation with someone who understands what you're going through, we're here.

References

Selerix, "COBRA Rules for Employers: Requirements & Deadlines." https://selerix.com/blog/cobra-rules-for-employers/

Centers for Medicare & Medicaid Services, "COBRA Continuation Coverage Questions and Answers." https://www.cms.gov/cciio/programs-and-initiatives/other-insurance-protections/cobra_qna

Centers for Medicare & Medicaid Services, "COBRA Continuation Coverage Questions and Answers." https://www.cms.gov/cciio/programs-and-initiatives/other-insurance-protections/cobra_qna

COBRA Insurance, "COBRA Insurance Cost." https://www.cobrainsurance.com/kb/how-much-does-cobra-insurance-cost/ — Taylor Benefits Insurance, "COBRA Costs 2024." https://www.taylorbenefitsinsurance.com/cobra-costs-2024/

UnitedHealthcare, "Health Insurance After a Spouse Dies." https://www.uhc.com/news-articles/benefits-and-coverage/health-insurance-after-a-spouse-dies

U.S. Department of Labor, "FAQs on HIPAA Portability and Nondiscrimination Requirements for Workers." https://www.dol.gov/sites/dolgov/files/EBSA/about-ebsa/our-activities/resource-center/faqs/hipaa-consumer-faqs.pdf

Capital Blue Cross, "CHIP Eligibility in Pennsylvania." https://www.capbluecross.com/wps/portal/cap/home/shop/chip/eligibility

Pennsylvania Department of Human Services, "CHIP Eligibility & Benefits FAQ." https://www.pa.gov/agencies/dhs/resources/chip/faq-chip/faq-chip-elibility-benefits

Pennsylvania Department of Human Services, "CHIP Eligibility and Benefits." https://www.pa.gov/agencies/dhs/resources/chip/eligibility-and-benefits

KFF, "I Didn't Sign Up for Part B When I First Became Eligible." https://www.kff.org/faqs/medicare-open-enrollment-faqs/general-enrollment-information/i-didnt-sign-up-for-part-b-when-i-first-became-eligible-but-want-to-sign-up-now-i-know-there-is-a-penalty-for-late-enrollment-is-there-any-way-to-avoid-the-penalty/

Medicare.gov, "Avoid Late Enrollment Penalties." https://www.medicare.gov/basics/costs/medicare-costs/avoid-penalties — AARP, "How Much Is the Late Enrollment Penalty for Medicare Part B?" https://www.aarp.org/medicare/how-much-is-the-part-b-late-enrollment-penalty/

AARP, "How Much Is the Late Enrollment Penalty for Medicare Part B?" https://www.aarp.org/medicare/how-much-is-the-part-b-late-enrollment-penalty/

Medicare.gov, "Avoid Late Enrollment Penalties." https://www.medicare.gov/basics/costs/medicare-costs/avoid-penalties — CMS, "Creditable Coverage and Late Enrollment Penalty." https://www.cms.gov/medicare/enrollment-renewal/part-d-plans/creditable-coverage-and-late-enrollment-penalty

SelectQuote, "Guide to Original Medicare for People Who Are Divorced or Widowed." https://www.selectquote.com/medicare/articles/original-medicare-for-people-who-are-divorced-or-widowed

MedigapSeminars, "Medicare for People Who Are Divorced or Widowed." https://medigapseminars.org/medicare-for-people-who-are-divorced-or-widowed/

Disclosure

Providers & Families Wealth Management has made every effort to ensure the accuracy of the information contained in this post. However, this content is provided for informational and educational purposes only and should not be relied upon as legal, tax, financial, or benefits advice. Health insurance rules, deadlines, and program eligibility are subject to change, and individual circumstances vary. Please consult a qualified attorney, benefits counselor, health insurance broker, or financial advisor regarding your specific situation.

External links are provided as a convenience and for informational purposes only. Providers & Families Wealth Management has no affiliation with any linked websites and makes no representations regarding the accuracy, completeness, or security of their content. We are not responsible for the content of external sites and do not endorse any products, services, or information found there.